AgendaVerified

This story is currently available in انگلیسی only — a translation isn't ready yet.

WTI jumps $2.70 to $92.15 as Iran risk repricing crowds out the inventory story

A 3.02% one-session move is a war premium, not a barrel-count move. The physical market has not tightened. The financial market has decided it might.

سرعت:

ℹ️ خواندن با صدای مرورگر · صدای استودیویی هوش مصنوعی بهزودی

SP

Sergei Petrov

· 3 min read

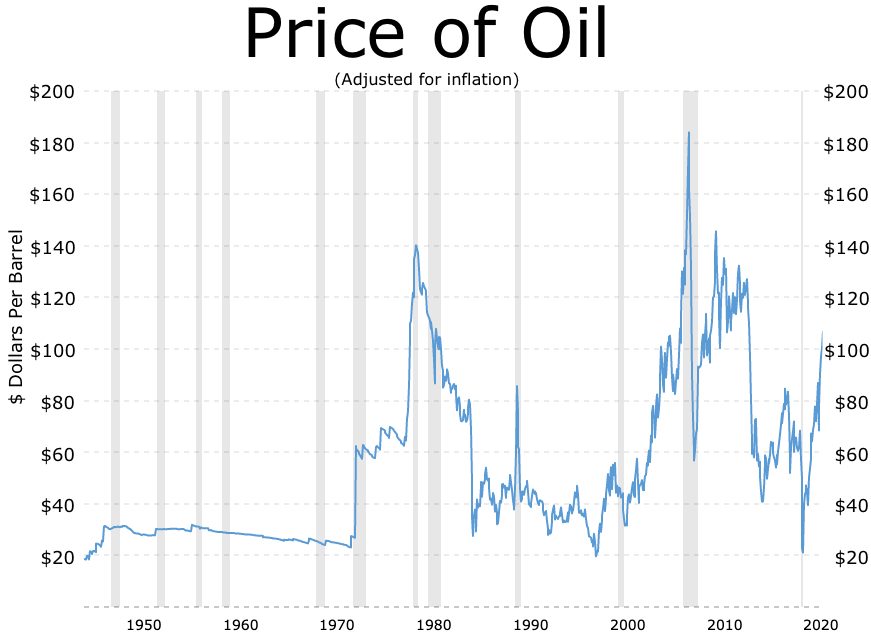

WTI crude settled at $92.15 per barrel on the morning of 28 May, up $2.70, or 3.02%, in a single session. That is a financial move, not a physical one. No pipeline shut overnight. No OPEC+ quota changed. No refinery in the Gulf reported an outage on the tape. The move is a repricing of geopolitical tail risk, and the tail in question is Iran.

The cause sits in the second paragraph, as it should. Reports over the past 72 hours describe an Iranian response posture following a confrontation that markets had until recently filed under containable. Commentary out of Washington and the Gulf is now framing a vengeful Iran as a scenario Riyadh did not want and did not plan for. The barrels are still the story. The politics are the cause.

Look at the three sides of the ledger.

**Supply:** nothing on the physical supply side has changed in the last 24 hours that justifies a three-dollar move on its own. Iranian exports continue to clear, sanctioned or not, via the usual ship-to-ship chains. Russian crude is still moving, though the failure of one sanctioned fuel tanker to reach Cuba after weeks at sea is a reminder that enforcement frictions are real and rising. OPEC+ discipline is intact, though the bloc is no longer the unified instrument it once was — the UAE's strained relationship with the quota framework has been on the wire again this week. None of that is new supply lost. It is supply that could be lost, which is a different ledger entry.

**Demand:** the demand side has not moved. Hajj-related travel into Saudi Arabia is at its seasonal peak, which supports regional jet and gasoline cracks but does not explain a global benchmark move of this size. Chinese buying behaviour, as filtered through the Astana-Beijing diplomatic traffic this week, suggests Kazakh and Central Asian barrels continue to find a home east. No demand surprise is doing the work here.

**Inventory:** this is where the column has to be honest. Commercial crude stocks in the OECD remain inside the five-year range. Floating storage is not flashing red. Strategic reserves in the U.S. are still well below the level of three years ago, which means the shock absorber is thinner than the headlines assume. That thinner cushion is part of why a risk-premium move of three dollars sticks rather than fades intraday. There is less inventory between the consumer and the next disruption than there was in the prior cycle.

The financial overlay deserves its own paragraph. The dollar weakened modestly against the rouble, with USD/RUB at 70.90, down 0.47 on the session. That is consistent with a risk-on commodity bid rather than a flight to the dollar, and it tells you the move in WTI is being led by length being added in crude futures, not by dollar mechanics. Henry Hub gas, at $3.076, was essentially unchanged at -0.29%. Gas is not participating. That is the cleanest tell that this is an oil-specific geopolitical bid, not a broad energy-complex repricing.

What to watch over the next five sessions. First, the weekly U.S. inventory print: if commercial crude draws more than the trade expects, the $92 handle becomes a floor rather than a ceiling. Second, any confirmed physical interruption — a tanker incident, an insurance withdrawal from Gulf transit, a refinery outage attributable to the standoff. That would convert the financial premium into a physical one, and the next leg would not be three dollars. Third, OPEC+ signalling. If the bloc indicates it will release barrels into a disruption, the premium compresses fast. If it stays silent, the market will assume the spare capacity is notional.